UAE businesses are scaling fast. According to PwC’s Global CEO Survey, 75% of CEOs in the UAE already have a defined AI roadmap, reflecting the aggressive investment in technology, vendors, and new operational systems.

But rapid investment creates a quieter challenge for finance leaders: spending visibility.

Budgets may look accurate during annual planning, yet once operations begin, costs start drifting. New SaaS tools emerge, vendor contracts expand, and departments incur expenses that were never part of the original plan.

For CFOs and finance teams, the real challenge isn’t building the budget; it’s maintaining spending discipline after the budget is approved.

This is where static budgets become critical. They establish fixed spending limits that help finance teams monitor departmental costs and detect variance before overspending spreads across the organisation.

TL;DR Key Takeaways

- Static budgets anchor predictable cost commitments. Finance teams apply them to expenses with contractual pricing, such as leases, enterprise software, vendor retainers, and compliance obligations.

- Department budgets rely on structural cost assumptions. Finance leaders build static budgets using workforce plans, procurement commitments, and historical cost behaviour.

- Static budgets act as governance tools. They establish cost ceilings that force departments to route new spending through finance approval.

- Variance analysis reveals cost drift early. Comparing actual spending against static budgets highlights vendor scope expansion, SaaS tool sprawl, and decentralised procurement.

- Spend visibility improves budget discipline. Platforms such as Alaan consolidate card transactions, invoices, and approvals into a single workflow, enabling finance teams to detect variance signals earlier.

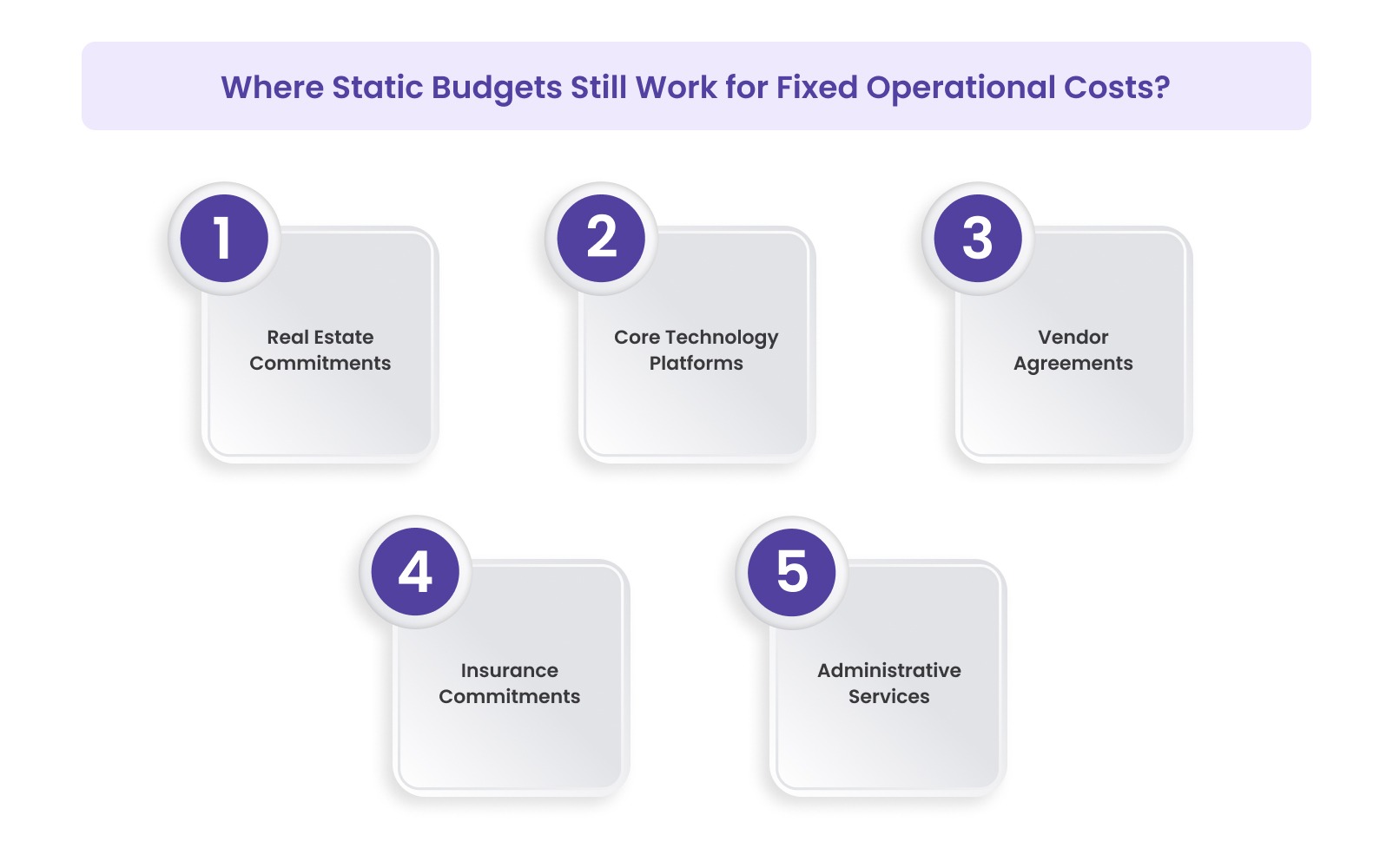

Where Static Budgets Still Work for Fixed Operational Costs?

Static budgets are useful mainly in areas where contracts limit how much operations can change costs. For finance leaders, the goal is to separate predictable obligations from spending that needs active management.

In practice, CFOs use static budgets to keep baseline costs stable while focusing analysis on expenses that affect margins, pricing, or working capital.

In UAE companies, static budgets usually cover commitments where pricing is locked by contract, VAT treatment stays consistent, and operational use doesn’t change the cost base.

Below are key points where static budgets still work for fixed operational costs.

1. Real Estate Commitments With Contract-Locked Pricing

Commercial leases are one of the few expenses with long-term contracts that make costs predictable. In the UAE, leases are often registered with Ejari, with payment schedules covering the full term.

Static budgets work well when:

- Lease agreements define fixed base rent for multiple years.

- Payment schedules follow the contractual instalments.

- Facility-related operating costs are separate from the base rent.

Finance teams still watch for early signs of change, like:

- Service charge adjustments from property managers.

- Maintenance or facility costs linked to building operations.

- Portfolio changes from workforce growth or office consolidation.

Many finance teams keep base rent under static budgets and track facility costs as variable overhead. This prevents day-to-day operational spending from affecting the stability of long-term real estate costs.

Suggested Read: Understanding and Analysing Real Estate Balance Sheet

2. Core Technology Platforms With Contractual Pricing

Technology expenses can be static only when pricing is defined by contract. Many technology costs, however, vary with licensing and workforce growth.

Static budgets are suitable when:

- Enterprise platforms have multi-year contracts with fixed pricing.

- Usage-based billing is minimal during the contract.

- Procurement authority for core systems is centralized under finance or IT.

CFOs watch for cost changes from:

- License expansion, which is faster than workforce growth.

- Departments that are buying overlapping SaaS tools.

- Contracts that scale with users or data.

According to PwC Middle East’s Digital and Technology Survey, organisations across the Middle East are increasing technology adoption while facing growing digital and technology risks. This highlights the need for strong governance and controls.

3. Vendor Agreements With Stable Service Scope

Vendor contracts can seem predictable when pricing is fixed, but cost stability depends on keeping the service scope unchanged.

Static budgets work when:

- Vendor pricing is fixed for the contract.

- Service scope doesn’t depend on operational use.

- Billing schedules are predictable, monthly or quarterly.

Finance teams watch for risks like:

- Scope expansions requested by departments.

- Contract renegotiations at renewal.

- Service upgrades that add charges.

In logistics and construction, vendor contracts often cover infrastructure like fleet maintenance. Static budgets stabilize these costs while procurement checks renewals to align pricing with margins.

4. Compliance and Insurance Commitments

Regulatory licenses and insurance usually renew on predictable annual cycles, making them suitable for static budgets during the policy period.

Static budgets apply when:

- Policies define fixed coverage costs for the year.

- Licenses follow scheduled renewals.

- Compliance obligations are mandated by law.

Finance teams reassess costs if:

- Regulations change across jurisdictions.

- Operations grow, and risk exposure increases.

- Coverage levels need to be adjusted during annual risk reviews.

In the UAE, teams also check vendor invoices for insurance or compliance to meet Federal Tax Authority requirements, including valid TRNs for VAT recovery.

5. Administrative Services Under Retainer Structures

Professional advisory services often use fixed retainers, making them fit for static budgets when the service scope stays stable.

Static budgets work when:

- Engagements run under fixed retainers.

- Payment structures stay constant.

- Deliverables are defined upfront.

Finance leaders watch for cost growth from:

- Additional advisory work outside the contract.

- Department-level consulting that bypasses procurement.

- Extended hours that increase billable costs.

Once you identify where static budgets still work for fixed operational costs, finance leaders can structure static budgets for departmental spending.

How Finance Leaders Structure Static Budgets for Departmental Spending?

Departmental static budgets rarely fail due to calculation errors. They fail when operational teams get lost in the assumptions made during annual planning.

For CFOs, managing departmental budgets is more about controlling how departments spend. Finance leaders set static budgets to define predictable cost boundaries while still allowing flexibility for operational growth.

In practice, static budgets work best when finance teams control procurement, vendor approvals, and hiring decisions.

Here’s how finance leaders structure static budgets for departmental spending:

1. Separate Structural Costs From Departmental Discretion

Finance leaders start by separating costs that departments cannot influence during the year. These represent the structural cost base of the organisation.

Common examples include:

- Workforce costs aligned with approved headcount plans

- Enterprise systems procured through central IT governance

- Long-term vendor contracts with fixed pricing

Challenges arise when discretionary spending becomes mixed with these structural costs, making overall budget management more difficult.

Discretionary actions that often create pressure include:

- New SaaS subscriptions outside the approved stack

- Consulting engagements arranged directly by teams

- Vendor payments processed without procurement approval

Many UAE companies face this when regional teams buy local services without central oversight. By isolating structural costs early, finance leaders preserve budget predictability.

2. Identify Early Signals of Departmental Budget Drift

Departments rarely exceed their budgets with a single decision. Cost pressure usually builds gradually through multiple small spending choices.

CFOs watch for signs like:

- Vendor payments outside procurement workflows

- Software spending that is growing faster than headcount

- Advisory or consulting costs appearing within operational teams

- Hiring beyond approved workforce plans

Many organisations trigger internal reviews when spending passes procurement thresholds or costs rise faster than revenue.

Example:

Dubai-based logistics operator DP World has invested heavily in integrated operational systems to manage suppliers and maintenance across its global ports. By centralising oversight, the company can track vendor performance, coordinate maintenance, and maintain cost control.

This helps prevent small, unchecked spending decisions from escalating into larger budget issues.

3. Align Department Budgets With Business Model Economics

Departmental budgets must reflect the business model’s economics, not just past spending. Finance leaders evaluate allocations against operational drivers such as:

- Revenue growth expectations

- Workforce expansion plans

- Procurement tied to operational capacity

Budget behaviour also varies by sector:

SaaS companies

- Engineering hiring and cloud costs grow with customer adoption

- Tech spending can rise before revenue stabilises

Logistics companies

- Fleet expansion adds maintenance and infrastructure costs

- Growing warehouse capacity creates extra vendor commitments

Construction firms

- Project mobilisation drives subcontractor and equipment costs

- Spending fluctuates with project pipelines and contract timelines

Aligning budgets with these drivers keeps cost assumptions realistic while protecting margins.

Also Read: How to Build a Business Budget for Your UAE Startup

4. Monitor Variance as an Operational Risk Signal

Variance analysis is an early warning system, not just a reporting exercise. Finance leaders track:

- Departments exceeding procurement limits

- Vendor contracts expanding beyond the original scope

- Operational costs that are rising faster than revenue

- Recurring expenses outside authorised cost centres

Finance teams also ensure that vendor invoices comply with Federal Tax Authority rules, including valid TRN details for VAT recovery. Maintaining ongoing visibility into departmental spending is essential for static budgets to remain effective.

To address this need, Alaan consolidates corporate card transactions, expense submissions, and approval workflows into a single platform. This enables finance leaders to:

- Detect vendor payments outside procurement rules

- Spot departmental spending over budget

- Enforce approval hierarchies before purchases

- Monitor cost behaviour across departments in real time

With this visibility, CFOs can act early and keep departmental budgets aligned with the organisation’s financial strategy.

Understanding how static budgets are structured helps explain why they continue to provide financial discipline across departments.

5 Reasons Why Static Budgets Still Provide Financial Discipline

Even as many finance teams adopt rolling forecasts and detailed planning, static budgets continue to play a vital role for UAE companies. Their primary value lies not in planning, but in governance: they establish clear spending limits in areas that should not expand without financial approval.

For CFOs, static budgets serve as a control mechanism, helping finance teams identify cost drift, enforce procurement rules, and protect operating margins.

The following reasons explain why static budgets remain essential for maintaining financial discipline.

1. Contain Operational Cost Drift Before It Escalates

In growing organisations, cost increases rarely happen through formal budget changes. They usually creep in through small operational decisions across teams.

Finance leaders watch for signals like:

- Departments introducing new SaaS tools outside approved stacks

- Marketing or consulting costs that are expanding mid-quarter

- Teams that are committing to vendor services without procurement approval

Static budgets set a fixed cost ceiling, forcing these decisions into formal financial review processes.

2. Protect Operating Margins During Vendor Cost Inflation

Vendor cost increases often appear gradually, through contract renegotiations or expanded service scopes.

Static budgets help finance leaders identify when supplier costs diverge from annual planning assumptions.

Teams typically monitor indicators like:

- Facility management vendors expanding service contracts mid-year

- Maintenance or support providers adding extra charges

- Logistics or operational suppliers renegotiating prices above inflation

3. Prevent Decentralised Procurement From Expanding Costs

As companies scale across regions or units, procurement often becomes fragmented.

Without clear budget limits, decentralised purchasing can create:

- Duplicate vendor contracts across departments

- Overlapping software tools across teams

- Local vendor agreements outside central procurement

This is common in UAE organisations with multiple locations, where regional teams contract vendors independently of headquarters.

Static budgets set financial boundaries that require departments to route new vendor commitments through the finance approval process.

4. Improve Forecast Stability for Structural Cost Commitments

Some operational costs are predictable across financial cycles and form the organisation’s structural cost base.

Examples include:

- Commercial property leases

- Enterprise technology licences

- Long-term vendor service contracts

Including these commitments in static budgets gives finance teams a stable baseline for forecasting operating expenses.

This stability lets CFOs focus forecasts on areas with more cost volatility, such as hiring, logistics, or discretionary spending.

5. Reinforce Financial Governance Across Departments

Static budgets work less as a planning tool and more as a framework for financial discipline.

They let finance leaders:

- Set clear cost limits for operational teams

- Enforce procurement approval before new spending

- Spot departmental cost behaviour that strays from strategy

While static budgets help maintain financial discipline, variance analysis reveals how closely actual spending aligns with these planned limits.

How Static Budget Variance Reveals Hidden Overspending?

Variance analysis offers a clear view of operational decisions that diverge from the assumptions underlying annual financial planning. Static budget variances, in particular, often expose cost behaviours that standard financial reports overlook.

By monitoring these variances closely, you can quickly identify areas where procurement discipline is weakening, vendor costs are increasing, or operational commitments are expanding faster than expected.

Below are the ways variance analysis reveals hidden spending patterns across departments.

1. Vendor Contracts Expanding Beyond Budget Assumptions

Vendor costs often exceed budget assumptions when operational teams expand service scope during the year.

Finance teams usually spot variance when:

- Service providers add deliverables outside the original contract

- Departments request extra support from retained vendors

- Operational teams renegotiate vendor services without updating budgets

Must Read: Vendor Payments in the UAE: Methods, Tools, and Best Practices

2. Technology Spend Growing Faster Than Workforce

Technology spending becomes a concern when it grows faster than the organisation’s operational scale.

Finance teams investigate variance when:

- SaaS costs rise without matching workforce growth

- Departments adopt specialised software outside central IT procurement

- Multiple teams use tools serving similar functions

This is common in UAE technology and e-commerce companies, where teams adopt platforms to solve immediate workflow needs.

Variance analysis helps finance teams identify when technology costs diverge from the approved budget.

At Alaan, corporate card transactions and expense submissions are recorded in real time, giving finance teams early visibility into software subscriptions and vendor payments before costs accumulate.

3. Operational Spending Expanding Faster Than Revenue

Operational costs become risky when they grow faster than the revenue they support.

Variance analysis often flags situations where:

- Sales travel expands faster than customer acquisition revenue

- Logistics or fulfilment costs rise faster than order volumes

- Teams increase service spending before revenue growth stabilises

4. Duplicate Vendor Relationships Across Departments

Variance analysis also shows when departments contract similar vendors independently.

Finance leaders detect this when:

- Multiple departments purchase similar consulting or advisory services

- Teams adopt overlapping software platforms

- Regional offices engage local vendors outside central procurement

Once detected, finance teams usually consolidate vendors or centralise procurement to prevent unnecessary duplication.

5. Financial Commitments That Appear After Budget Approval

Some operational commitments are approved long before they appear in financial reports.

Variance analysis helps identify situations where:

- Departments approve vendor engagements that only start billing later

- Service expansions are agreed operationally, but not reflected in budgets

- Procurement commitments appear only once invoices are issued

When these costs hit financial records, they can push departmental spending above approved limits. Finance teams use variance signals to trace these changes back to the operational decisions that created them.

The insights from budget variance analysis help finance teams decide whether a static or flexible budgeting approach best fits their organisation.

Static vs Flexible Budgets: How Finance Teams Decide the Right Model

Finance leaders rarely view static and flexible budgets as competing approaches. In practice, most organisations use both simultaneously, applying each depending on how closely costs track operational activity.

The key consideration is determining which costs require tight control and which should scale with business performance. By carefully applying static and flexible budgets, finance leaders can guide spending decisions without hindering the insights needed for day-to-day operations.

In practice, many organisations still depend on static budgets, making effective control and monitoring critical for finance teams.

How Alaan Helps Finance Teams Maintain Control Over Static Budgets?

Many finance teams set annual budgets, yet operational spending often happens across multiple cards, vendor invoices, and disconnected systems. When spending data is fragmented, finance leaders lose visibility into how departmental costs evolve during the year.

This delay makes it hard to spot when operational spending starts diverging from approved static budgets.

At Alaan, we bring corporate cards, expense capture, approval workflows, and accounting integrations into one spend management platform. Finance teams gain real-time visibility into operational spending, enabling them to detect budget variances early and enforce stronger financial governance across departments.

What Alaan Covers Across the Operational Spend Lifecycle

Maintaining discipline within static budgets depends on controlling operational spending consistently before, during, and after expenses occur. At Alaan, we support finance teams at every stage of the spend lifecycle, helping them enforce budget policies, detect variance signals early, and keep financial records accurate.

1. Corporate Cards With Built-In Spend Controls

At Alaan, we provide corporate cards with configurable policy controls that let finance teams manage spending before financial commitments happen.

Finance teams can:

- Set spending limits by employee, department, or project

- Restrict merchant categories outside the company policy

- Issue virtual or physical cards instantly when needed

- Freeze or block cards in real time if unusual spending occurs

These controls help finance leaders prevent spending that could exceed approved static budgets.

2. Automated Expense Capture for Accurate Budget Monitoring

Operational expenses are automatically recorded as transactions occur, ensuring finance teams capture data without delays.

At Alaan, we extract key transaction details like:

- Vendor name

- Transaction amount

- Invoice date

This structured data lets finance teams categorise spending accurately and analyse departmental costs against approved budgets. Accurate expense classification also improves the reliability of variance analysis during financial reviews.

3. Policy-Based Approvals for Budget Governance

Expenses go through structured approval workflows in line with internal spending policies.

Typical approvals include:

- Department heads reviewing expenses within their budget

- Finance leaders reviewing higher-value transactions or vendor commitments

These controls ensure departments can’t introduce new spending without proper oversight. This is especially important when teams try to expand vendor contracts or add operational costs midyear.

4. Real-Time Visibility Into Departmental Spending

Finance leaders gain real-time insight into operational spending across departments.

Dashboards let teams monitor:

- Corporate card transactions across teams

- Submitted expenses and supporting documents

- Departmental spending trends

- Pending approvals

This visibility makes it easy to compare spending against approved static budgets and spot early signs of cost drift.

5. Real-Time Budget Monitoring Across Departments

Because operational spending data is captured continuously, you gain a clearer view of how departmental budgets are being used throughout the year.

This allows you to:

- Identify budget variances early

- Monitor vendor spending patterns

- Track operational commitments across departments.

Better visibility helps finance leaders maintain financial discipline while supporting operational growth.

What Alaan Is (And Is Not)

Alaan is a spend management platform designed to strengthen financial control over operational spending.

It helps finance teams:

- Enforce spending policies across departments

- Maintain visibility into operational expenses

- Improve the accuracy of financial reporting

Alaan is not accounting software. Instead, it integrates with existing accounting and ERP systems like NetSuite, QuickBooks, Xero, and Microsoft Dynamics.

By strengthening upstream spend control, Alaan helps finance teams maintain accurate financial records and monitor departmental budgets more effectively.

Final Thoughts

Static budgets give finance teams a stable reference point for monitoring predictable operating costs. But budget discipline rarely fails at the planning stage. It breaks down when operational spending increases due to vendor commitments, departmental purchases, or decentralised procurement decisions during the financial year.

Without continuous visibility into these transactions, finance leaders often detect cost drift only during monthly reporting cycles, when departmental spending has already moved beyond the assumptions used during planning.

At Alaan, we help finance teams maintain that visibility by bringing corporate card transactions, expenses, approvals, and receipt data into a single controlled workflow. This allows finance leaders to monitor departmental spending in real time, detect variance signals earlier, and enforce procurement policies before operational costs expand beyond approved budgets.

Schedule a free demo to see how Alaan helps UAE businesses strengthen spend visibility, maintain budget discipline, and manage operational expenses with greater financial control

FAQs

1. When should finance teams use a static budget?

Finance teams typically use static budgets for salaries, office leases, long-term vendor contracts, and fixed software subscriptions, where spending does not change significantly with operational activity.

2. What factors should finance leaders consider before using a static budget?

Finance leaders should assess cost predictability, operational dependency, and business growth plans. Static budgets work best when spending remains stable, but they become less reliable when costs change due to hiring expansion, new projects, or usage-based technology expenses.

3. How do finance teams calculate static budget variance?

Finance teams calculate static budget variance by comparing actual spending with the approved static budget for a department or cost category. This comparison helps identify where departments are exceeding planned limits and where spending remains within the approved budget.

4. What are the limitations of static budgets for growing organisations?

Static budgets become less effective when departmental spending increases due to hiring, new projects, or variable operational costs. In these situations, the original annual budget may no longer reflect the department’s actual cost structure.

5. Can static budgets and flexible budgets be used together?

Yes. Many finance teams use static budgets for predictable operational costs, such as salaries and facilities, while using flexible budgets for variable expenses, such as marketing campaigns, logistics, and cloud infrastructure usage.